“Economics is the social science that describes the factors that determine the production, distribution and consumption of goods and services.”

(Source: Wikipedia)

The Nature of the Economic Problem

Resources: are the inputs required for the production of goods and services.

Scarcity: a lack of something (in this context, resources).

The fundamental economic problem is that there is a scarcity of resources to satisfy all human wants and needs. There are finite resources and unlimited wants. This is applicable to consumers, producers, workers and the government, in how they manage their resources.

Economic goods are those which are scarce in supply and so can only be produced with an economic cost and/or consumed with a price. In other words, an economic good is a good with an opportunity cost. All the goods we buy are economic goods, from bottled water to clothes.

Free goods, on the other hand, are those which are abundant in supply, usually referring to natural sources such as air and sunlight.

The Factors of Production

Resources are also called ‘factors of production’ (especially in Business). They are:

- Land: all natural resources in an economy. This includes the surface of the earth, lakes, rivers, forests, mineral deposits, climate etc.

- The reward for land is the rent it receives.

- Since, the amount of land in existence stays the same, its supply is said to be fixed. But in relation to a country or business, when it takes over or expands to a new area, you can say that the supply of land has increased, but the supply is not depended on its price, i.e. rent.

- The quality of land depends upon the soil type, fertility, weather and so on.

- Since land can’t be moved around, it is geographically immobile but since it can be used for a variety of economic activities it is occupationally mobile.

- Labour: all the human resources available in an economy. That is, the mental and physical efforts and skills of workers/labourers.

- The reward for work is wages/salaries.

- The supply of labour depends upon the number of workers available (which is in turn influenced by population size, no. of years of schooling, retirement age, age structure of the population, attitude towards women working etc.) and the number of hours they work (which is influenced by number of hours to work in a single day/week, number of holidays, length of sick leaves, maternity/paternity leaves, whether the job is part-time or full-time etc.).

- The quality of labour will depend upon the skills, education and qualification of labour.

- Labour mobility can depend up on various factors. Labour can achieve high occupational mobility (ability to change jobs) if they have the right skills and qualifications. It can achieve geographical mobility (ability to move to a place for a job) depending on transport facilities and costs, housing facilities and costs, family and personal priorities, regional or national laws and regulations on travel and work etc.

- Capital: all the man-made resources available in an economy. All man-made goods (which help to produce other goods – capital goods) from a simple spade to a complex car assembly plant are included in this. Capital is usually denoted in monetary terms as the total value of all the capital goods needed in production.

- The reward for capital is the interest it receives.

- The supply of capital depends upon the demand for goods and services, how well businesses are doing, and savings in the economy (since capital for investment is financed by loans from banks which are sourced from savings).

- The quality of capital depends on how many good quality products can be produced using the given capital. For example, the capital is said to be of much more quality in a car manufacturing plant that uses mechanisation and technology to produce cars rather than one in which manual labour does the work.

- Capital mobility can depend upon the nature and use of the capital. For example, an office building is geographically immobile but occupationally mobile. On the other hand, a pen is geographically and occupationally mobile.

- Enterprise: the ability to take risks and run a business venture or a firm is called enterprise. A person who has enterprise is called an entrepreneur. In short, they are the people who start a business. Entrepreneurs organize all the other factors of production and take the risks and decisions necessary to make a firm run successfully.

- The reward to enterprise is the profit generated from the business.

- The supply of enterprise is dependent on entrepreneurial skills (risk-taking, innovation, effective communication etc.), education, corporate taxes (if taxes on profits are too high, nobody will want to start a business), regulations in doing business and so on.

- The quality of enterprise will depend on how well it is able to satisfy and expand demand in the economy in cost-effective and innovative ways.

- Enterprise is usually highly mobile, both geographically and occupationally.

All the above factors of productions are scarce because the time people have to spend working, the different skills they have, the land on which firms operate, the natural resources they use etc. are all in limited in supply; which brings us to the topic of opportunity cost.

Opportunity Cost

The scarcity of resources means that there are not sufficient goods and services to satisfy all our needs and wants; we are forced to choose some over the others. Choice is necessary because these resources have alternative uses- they can be used to produce many things. But since there are only a finite number of resources, we have to choose.

When we choose something over the other, the choice that was given up is called the opportunity cost. Opportunity cost, by definition, is the next best alternative that is sacrificed/forgone in order to satisfy the other.

Example 1: the government has a certain amount of money and it has two options: to build a school or a hospital, with that money. The govt. decides to build the hospital. The school, then, becomes the opportunity cost as it was given up. In a wider perspective, the opportunity cost is the education the children could have received, as it is the actual cost to the economy of giving up the school.

Example 2: you have to decide whether to stay up and study or go to bed and not study. If you chose to go to bed, the knowledge and preparation you could have gained by choosing to stay up and study is the opportunity cost.

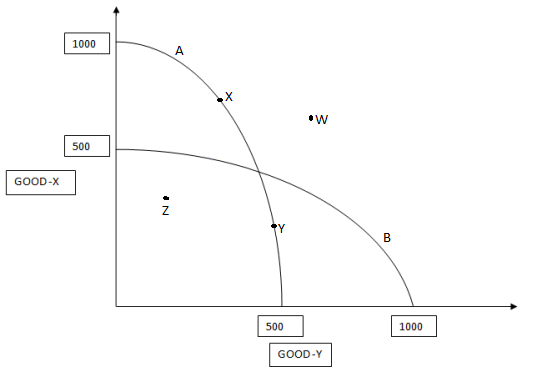

Production Possibility Curve Diagrams (PPC)

Because resources are scarce and have alternative uses, a decision to devote more resources to producing one product means fewer resources are available to produce other goods. A Production Possibility Curve diagram shows this, that is, the maximum combination of two goods that can be produced by an economy with all the available resources.

The PPC diagram above shows the production capacities of two goods- X and Y- against each other. When 500 units of good X are produced, 1000 units of good Y can be produced. But when the units of good X increases to 1000, only 500 units good Y can be produced.

Let’s look at the PPC named A. At point X and Y it can produce certain combinations of good X and good Y. These are points on the curve- they are attainable, given the resources. Th economy can move between points on a PPC simply by reallocating resources between the two goods.

If the economy were producing at point Z, which is inside/below the PPC, the economy is said to be inefficient, because it is producing less than what it can.

Point W, outside/above the PPC, is unattainable because it is beyond the scope of the economy’s existing resources. In order to produce at point W, the economy would need to see a shift in the PPC towards the right.

For an outward shift to occur, an economy would need to:

- discover or develop new raw materials. Example: discover new oil fields

- employ new technology and production methods to increase productivity

- increase labour force by encouraging birth and immigration, increasing retirement age etc.

An outward shift in PPC, that is higher production possibility, will lead to economic growth.

In the same way, an inward shift can occur in the PPC due to:

- natural disasters, that erode infrastructure and kill the population

- very low investment in new technologies will cause productivity to fall over time

- running out of resources, especially non-renewable ones like oil or water

An inward shift in the PPC will lead to the economy shrinking.

How is opportunity cost linked to PPC?

Individuals, businessmen and the government can calculate the opportunity cost from PPC diagrams. In the above example, if the firm decided to increase production of good Y from 500 to 750, it can calculate the opportunity cost of the decision to be 250 units of good X (as production of good X falls from 1000 to 750). They are able to compare the opportunity cost for different decisions.

Notes submitted by Lintha

Click here to go to the next topic.

Click here to go back to the Economics menu.

Thanks for the notes but what about utility?

LikeLike

‘Utility’ is not covered in IGCSE Economics (0455).

LikeLike

what about durable and non-durable goods?

LikeLike

That distinction is not important to this unit. You can of course use it in your exams if you want.

LikeLike

I really like your notes

LikeLiked by 3 people

I am a youtuber and make videos of economic so may i take the help of these

Great Notes

Thank you .

LikeLiked by 1 person

These notes are protected by copyright, so I would advise against using large chunks of them, but quoting small lines or referencing our notes should be fine, provided that you give us the necessary credit!

Thank you so much for asking, by the way 🙂

LikeLike

Will it help if I only study these notes for an exam??

LikeLike

Will reading and

memorising only these help before my exams or should I even do my textbook?

LikeLike

Don’t memorise! Understand the concepts and frame your own answers. These are revision notes, so you shouldn’t rely on these as the only study reference. Learn from the textbook first and use these notes to revise before the exams.

LikeLiked by 1 person

do your textbook too. Try memorizing it and applying it ( by trying questions from your textbook or online resources.)

LikeLike

Thank you for these notes, quite helpful!

LikeLike

Welcome!!

LikeLike

Are these notes able to be downloaded as a pdf?

LikeLiked by 1 person

Not currently. We are, however, working on downloadable and printable versions of our notes that are available for purchase. If you are interested, stay tuned!

LikeLike

Informitive post. Thanks!

LikeLike

Fabulous notes

Thank You!!!

It helped me finish a chapter really fast

LikeLike

Glad we could help!

LikeLike

the new textbook that most IGCSE students are following is here:

https://www.snapdeal.com/product/cambridge-igcse-and-o-level/638329370736?gclid=CjwKCAjw1f_pBRAEEiwApp0JKOodntAbFTtgjv41tyGgNvNlIaEm6HN7Fy7tDVJHeD3xfs9aTDh_mBoCoCcQAvD_BwE&supc=SDL774300854&utm_source=earth_web&utm_medium=614_1515&utm_content=638329370736&vendorCode=Seb79d&isSellerPage=true&fv=true&utm_source=earth_pla&utm_campaign=40-60_nm&utm_term=70802652213&utm_medium=70802652213&s_kwcid=AL!660!3!352864509795!!!g!411540340457!&ef_id=XMMmDgAAEfa1b8Fc:20190730153031:s

so sorry for all the trouble

LikeLike

could you please add the notes for macro and microeconomics.

pls as I am having great trouble searching for it all over the internet.

thanks in advance

LikeLiked by 1 person

It is available here. https://igcseaid.com/notes/economics-0455/2-1-2-9-how-markets-work/

LikeLike