Accounts are the financial records of a firm’s transactions.

Final Accounts are prepared at the end of the financial year and give details of the profit or loss made as well as the worth of the business.

Profit

Profit = Sales Revenue – Total cost

When the total costs exceed the sales revenue, then a loss is made.

How to increase profit?

- Increase sales revenue

- Cut costs

Why is profit important to a business?

- It is a reward for enterprise: entrepreneurs start businesses to make a profit

- It is a reward for risk-taking: entrepreneurs has to take considerable risks when they invest capital in a venture, and profits are a compensation/reward to them for taking these risks (paid in the form of profits or dividends)

- It is a source of finance: after payments to owners, profits are reinvested back into the business for further expansion (this is called retained earnings)

- It is an indicator of success: more profits indicate to investors that the business/industry is worth their time and money, and they will invest more either int he firm or new firms of their own, in the hopes of gaining good returns on their investment

For social enterprises, profit is not one of their primary objectives, but welfare of the society is. However, they will also strive to make some profit to reinvest it back into the business and help it grow.

Profit is not the same as cash flow! Profit is the surplus amount after total costs have been deducted from sales. It includes all income and payments incurred in the year, whether already received or paid or to not yet received or paid respectfully. In a cash flow, only those elements paid in cash immediately are considered.

Income Statement

An income statement is a financial document of the business that records all income generated by the business as well as the costs incurred by the business and thus the profit or loss made over the financial year. Also known as profit and loss account.

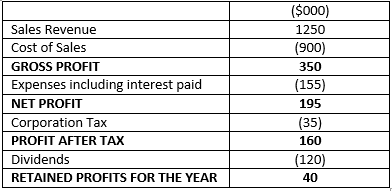

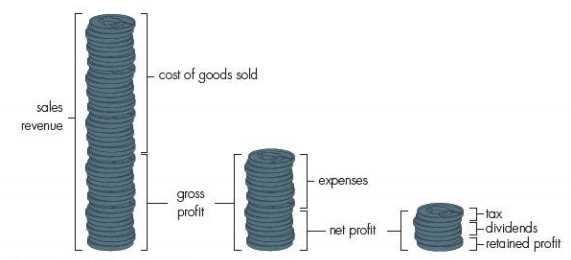

Sales Revenue = total sales

Cost of Sales = total variable cost of production + (opening inventory of finished goods – closing inventory of finished goods)

Gross Profit = Sales Revenue – Cost of Sales

Expenses: all overheads/fixed costs

Net Profit = Gross Profit – Expenses

Profit after Tax = Net Profit – Tax

Dividends: share of profit given to shareholders; return on shares

Retained Profit for the year = Profit after Tax – Dividends. This retained earnings is then kept aside for use in the business.

Uses of Income Statement

Income statements are used by managers to:

- know the profit/loss made by the business

- compare their performance with that of previous years’ and with that of competitors’. If profit is lower than that of last year’s why is it falling and what can they do to correct the issue? If it is lower than that of competitors’ what can they do to be more profitable and be competitive in the market?

- know the profitability of individual products by preparing separate income statement for each product. They may decide to stop production of products that are making losses.

- help decide what products to launch by preparing forecast income statement for the first few years. Whichever product is forecast to have a higher profit, the business will choose to launch that product

Notes submitted by Lintha

Click here to go to the next topic

Click here to go back to the previous topic

Click here to go back to the Business Studies menu

This website is really good and helping me as well with all my notes…over all I don’t want to right same lines copying from my book so…I use this notes as they even give me some another ideas which aren’t in the books…👍🏻

LikeLike

tREE

LikeLike

This has helped us a lot during our classes.

LikeLike